| |

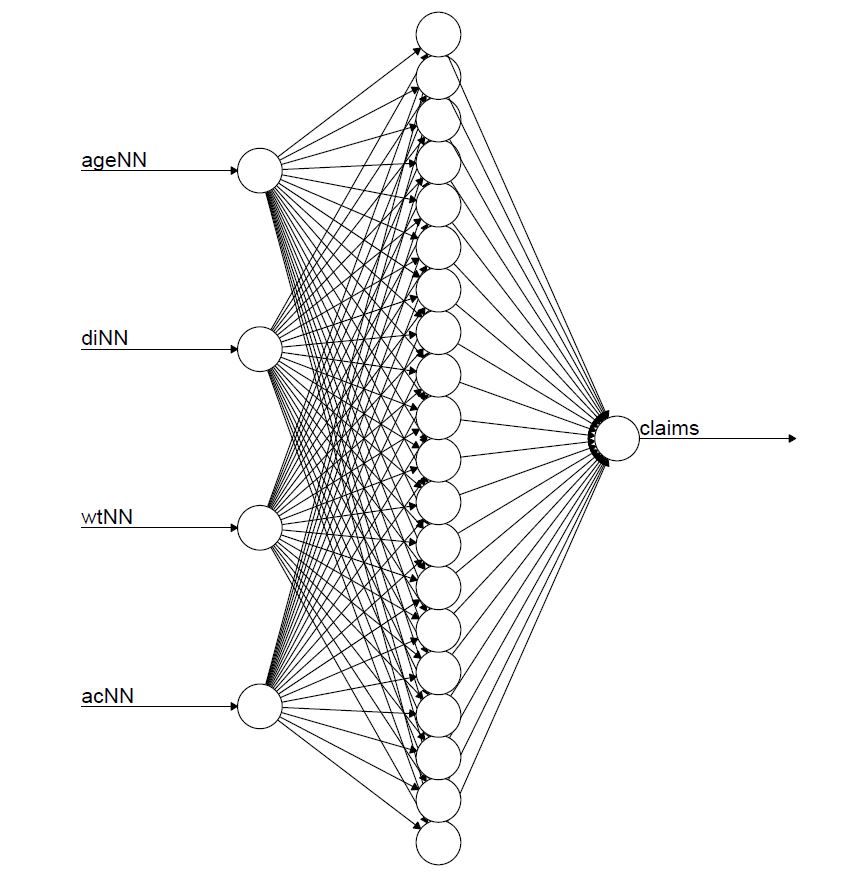

Individual Claims Generator: Monthly Cash Flows

We provide a fully calibrated stochastic generator of individual insurance claim developments in non-life insurance. We use the statistical computing software R. The cash flows and the claim closing processes are simulated on a monthly grid, they are covariate dependent, and they allow for claim re-openings and claim recoveries.

For a description of the generated data:

Individual claims generator for claims reserving studies: data simulation.R

(with M. Wang). SSRN Manuscript ID 4127073, 2022.

▸ GitHub repository (for download)

|

|

| |

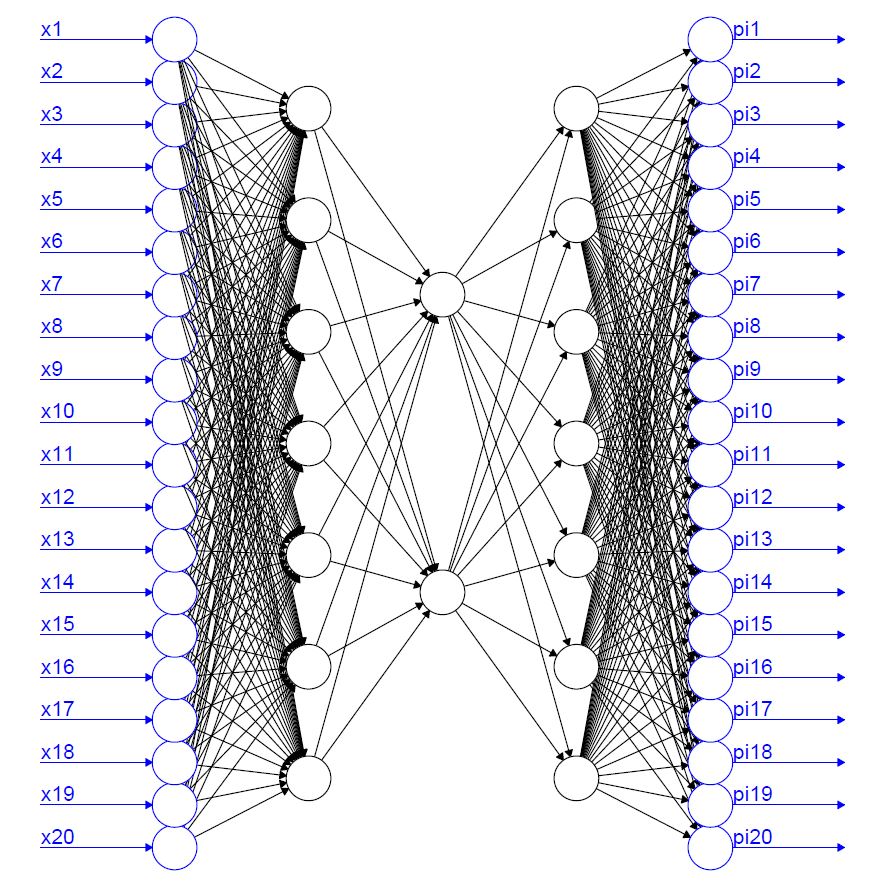

Individual Claims History Simulation Machine: Annual Cash Flows

We provide a fully calibrated simulation machine that allows one to simulate individual claims histories of non-life insurance claims. These claims histories depend on individual claims features, such as the age of the injured, and the resulting simulations provide reporting delays, individual cash flow patterns as well as the claims closing processes.

For a description of the R package:

Readme.pdf

For mathematical details we refer to the following reference:

An individual claims history simulation machine

(with A. Gabrielli). Risks 6/2 (2018), 29.

▸ Simulation Machine (Version 1) (zip download)

For further reading:

Back-testing the chain-ladder method

(with A. Gabrielli). Annals of Actuarial Science 13/2 (2019), 334--359.

Neural network embedding of the over-dispersed Poisson reserving model

(with A. Gabrielli and R. Richman). Scandinavian Actuarial Journal 2020/1 (2020), 1--29.

|

|

| |

v-a Heatmap Simulation Machine

We provide an R code that allows to simulate (synthetic) v-a heatmaps of individual car drivers in the

speed bucket (5,20]km/h. This simulation machine is based on a neural network architecture which has been calibrated to real GPS car driving data.

The scale has been chosen rather coarse for computational reasons. For mathematical details we refer to the following reference:

Feature extraction from telematics car driving heatmaps

(with G. Gao). European Actuarial Journal 8/2 (2018), 383--406.

▸ Simulation Machine (Version 1) (zip download)

For further reading:

Claims frequency modeling using telematics car driving data

(with G. Gao, S. Meng). Scandinavian Actuarial Journal 2019/3, 143--162.

Convolutional neural network classification of telematics car driving data

(with G. Gao). Risks 7/1 (2019), 6.

Clustering driving styles via image processing

(with R. Zhu). Annals of Actuarial Science 15/2 (2021), 276--290.

|

|